First published in June 2021. We highly recommend you start with Part I.

The Hudson Labs Red Flag Guide (Part II)

Revenue

Cash may still be king, but revenue is the it-girl on the cover of every tabloid. Revenue doesn’t just make the news, it is the headline. The attention paid to revenue provides a strong incentive to make sure it always looks good.

There are many ways to misrepresent a company’s revenues, including fake transactions, booking revenue too early, underestimating returns, recording one-time gain as revenue, and more.

To compound the revenue problem, the accounting is complicated. The general rule is that you may recognize revenue once you have fulfilled your obligation to the customer, but this isn’t always as simple as it seems.

Following the ice cream truck down the rabbit hole:

**(tl;dr - it is complicated) Pretend that you are the successful proprietor of an ice cream truck. Revenue accounting will be easy, right? Right? Consider a few scenarios:

- A customer buys a single cone for $5 and pays cash. You own the ice cream, the customer can’t return an ice cream cone.

**Great job, that’s $5 in revenue. 2. You are an independent contractor, and have an ice creams sales commission agreement with an ice cream company. For each $5 ice cream you sell you keep $2 and pay the ice cream company $3.

**Depending on your contract with the vendor you may have $5 revenue and $3 cost of sales, or you may have $2 net revenues (no cost of sales). Professional judgment is required in interpreting contract terms. **Similarly, the ice cream company may record $3 revenue, or $5 revenue and $2 cost of sales depending on the wording of your contract. They may recognize the sale when you pick-up the ice cream, only after you’ve sold it, or based on estimates of returns of unsold ice cream. 3. A customer comes up and buys a $5 ice cream using a $25 gift card. The amount of revenue you recognize is somewhere between $5 and $25, depending on your “breakage rate”. Breakage relates to gift card balances that are never used. Let’s assume that for every $25 of gift cards you sell, $5 will never be used: you have a breakage rate of $5 (never used) / $20 (will be used) = 25%. You are allowed to recognize a portion of the breakage as revenue as the gift card is spent.

**So you can recognize $5 for ice cream sold PLUS 25% of $5 (= $1.25) for breakage, for total revenue of $6.25. Changing your breakage rate changes your revenue, and your customer never knows the difference. **(end tl;dr) Selling the exact same ice-cream cone to the same customer for $5 gave revenues ranging from $2 to $6.25. The complexity is enough to make you open your deep freeze and sample the goods.

Increasing the complexity of the business increases the complexity of revenue recognition. Becoming a revenue expert is not a simple task. But all is not lost - you don’t need to be an expert to understand risks.

Look out for areas that include management estimates in revenue recognition (percent completed, estimated returns, breakage, etc…) and look out for changes in these estimates, look out for changes in policy, and look out for revenue concentration (only a few major customers). Common revenue manipulation schemes:

- Channel stuffing: Shipping or delivering more product than the customer or reseller ordered or needs. Companies with long-standing relationships with a few major customers are at a greater risk of channel stuffing, as are companies that use resellers, fulfillment centers and third-party distributors.

- Round-trip transactions: You pay me for services, I pay you for services, we both book revenue and expenses. There is no profit, no real value is created, but we both get to show plenty of growth.

- Sweetening the deal: Extending payment terms to cater to customers who might never pay or providing incentives to encourage customers to order now instead of later.

- Booking gains through revenue: Including one-time or non-recurring gains in revenue.

Look out for dramatic increases in revenue year-over-year. If revenue trends seem too good to be true, they might be just that.

Our algorithms extracted these interesting disclosures:

SOS Inc (SOS) | (20-F December 2020) had very impressive revenue growth but it was almost entirely attributable to only two client.

“97.9% of our revenues generated in the twelve months ended December 31, 2020 are from our insurance marketing business, of which we rely on two key clients or agents to dispatch insurance data mining business to us.”

General Electric Co (GE) | (10-Q | March 2021) reported 5% revenue growth in their GE Capital segment even though their sales volume decreased. The revenue growth was due to lower impairment estimates.

“GE Capital revenues increased 5%, primarily as a result of lower marks and impairments primarily in Insurance, partially offset by lower revenue at WCS due to lower volume and lower gains and project revenues at EFS.”

Clene Inc (CLNN | 10-Q | March 2021) was mentioned in our discussion of Related Party transactions in Part I. In their first quarter of 2021 they had about $0.2M in revenues, all from related parties. They paid related parties about $0.2M as a cost of product for the same transactions. It’s not clear why they needed to be involved in the transaction, but it certainly didn’t hurt for this new SPAC graduate to show significant revenue growth while waiting for FDA approvals for their other products.

Mergers & acquisitions

Many infamous accounting scandals have relied on acquisitions to mislead investors, including Valeant, Waste Management, CUC/Cedant, and WorldCom.

Acquisition accounting provides opportunities for manipulation, and frequent acquisitions provide frequent opportunities for manipulation. Of course, not all serial-acquirers commit fraud, but where there is opportunity there is heightened risk.

Why is acquisition accounting so susceptible to manipulation?

- Financial metrics, including revenues, become harder to compare year-over-year. Incorporating the financials of a newly acquired company can mask deteriorating performance in the original business.

- Significant costs incurred during the year can be ascribed to the acquisition, termed “non-recurring” and excluded from the key metrics presented to investors.

- In acquisition accounting, assets and liabilities are revalued to their fair value at the date of acquisition...

- Fair value isn’t always easy to ascertain. It is much harder to value a brand name or palladium mine than to value real estate in Manhattan. Valuations often include estimates, and estimates provide opportunities for manipulation.

- Companies can capitalize certain items, such as customer lists, when they are purchased. If generated internally, costs would need to be expensed immediately if generated internally. Acquiring these assets lets companies defer expenses to future periods.

- Finally, if you paid more than the fair value of identifiable assets and liabilities, you get to book the remainder as Goodwill. Goodwill stems from the assumption that buyers don’t voluntarily overpay, so the purchase price that can’t be allocated to identifiable assets must relate to unidentifiable assets. Goodwill does not depreciate in value, unless it is later found to be impaired. This means that unlike most assets, Goodwill does not have an expense component. Managers have an incentive to over-allocate purchased asset values to Goodwill and other intangibles whose values don’t have to be amortized. Goodwill impairment is another area involving significant management judgment.

Non-GAAP metrics, exclusions & one-time charges

If you’ve made it this far, you know that there is a fair amount of flexibility in accounting rules.

Even so, companies often present metrics not governed by accounting rules, non-GAAP metrics. The use of non-GAAP metrics is pervasive, with most companies reporting Earnings before interest, tax, and depreciation and amortization (EBITDA), Adjusted EBITDA, or some other non-GAAP income.

In theory, non-GAAP metrics are supposed to make earnings “comparable” by normalizing for differences in financing structures, tax rates, and major purchases, and non-recurring events. While it can be useful to look at normalized results, these metrics tend towards hypotheticals: “if not for a major class action lawsuit settlement and severance costs from significant layoffs, we would have been profitable”; “if not for the rain, it would have been a wonderful parade”. There is predictive power in the aggressiveness and the extent to which costs are excluded from non-GAAP metrics. Never disregard an expense item just because management is instructing you to.

This peculiar non-GAAP estimate was recently extracted by our Bedrock AI algorithms:

($PGEN | 10-Q | March 2021) “During the three months ended March 31, 2021, the Company modified the definition of Segment Adjusted EBITDA to exclude the gain or loss on disposals of assets and include proceeds from the sale of assets in the period sold." In theory, under this scheme, they could buy an asset for $3M, sell it at a loss for $1M and show $1M adjusted EBITDA profit, rather than a $2M adjusted EBITDA loss.

In creating their non-GAAP metrics, many companies often exclude expenses they describe as “special”, “one-time” or “non-recurring”. Very few expenses are truly one-time. Many companies undergo “restructuring” nearly every year but continue to insist this year’s expense is special.

While it may be the case that, for example, costs related to acquisitions are one-time events, serial-acquirers have acquisition costs every period. These companies certainly aren’t excluding their revenue bump from operations from EBITDA, yet they are excluding their costs to acquire those revenues.

Bally’s Corp ($BALY | 10-Q | March 2021) has been making multiple acquisitions each quarter and excludes costs related to acquisitions from Adjusted EBITDA in earning reports. In Q1 2021 they reported an accounting loss of $11 million, and an Adjusted EBITDA (profit) of $52 million.

If a company’s accounting (GAAP) earnings are consistently shrinking but their non-GAAP earnings are consistently growing, there is a problem. This is surprisingly common.

Reserves, accruals & allowances

Reserves, accruals and allowances are an area of accounting that require substantial management judgment.

The basic idea is that companies need to record accruals/reserves and corresponding expenses for costs they are obligated to pay (e.g. expected warranty repairs, customer returns, and expected product recalls), and need to record allowances for known future losses (e.g. inventory that will need to be deeply discounted, receivables for customers who may not pay). Changes in reserve, accrual, and allowance estimates often have a material effect on financial statements. General Electric ($GE) has a reputation for aggressive use of reserves:

(SEC Press Release| December 9, 2020) “The Securities and Exchange Commission today announced that General Electric Co. (GE) has agreed to pay a $200 million penalty to settle charges for disclosure failures in its power and insurance businesses. In 2017 and 2018, GE’s stock price fell almost 75% as challenges in its power and insurance businesses were disclosed to the public."

According to the SEC’s order, GE misled investors by describing its GE Power profits without explaining that one-quarter of profits in 2016 and nearly half in the first three quarters of 2017 stemmed from reductions in its prior cost estimates.

The discretion involved in these estimates provides an opportunity for earning manipulation.

- Over-allocation to reserve accounts during really good quarters gives you leeway to release reserves in bad quarters to consistently beat earnings estimates.

- Over-allocations are common in particularly bad years as well. If a company is restructuring or disposing of a line of business there is a temptation to over-accrue as the costs can be “normalized” as non-recurring in non-GAAP metrics.

When these costs are reversed in future periods it looks as though the company has orchestrated a highly successful recovery.

Impairment

Impairment occurs when the carrying value of an asset on the company’s balance sheet exceeds the true value of the asset. The true value or “fair value” is often difficult to estimate and involves significant management judgment.

Companies can avoid recording impairment if they can convince their auditors that the impairment is temporary.

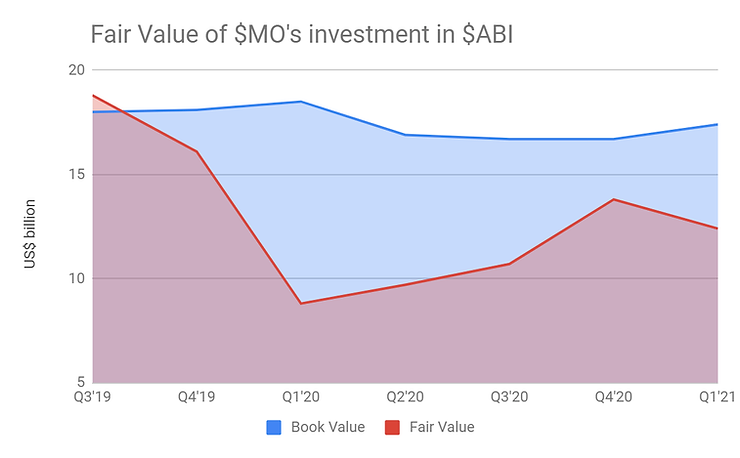

($MO | 10-Q | March 2021) “In October 2019, the fair value of Altria’s equity investment in ABI declined below its carrying value and has not recovered. Altria has evaluated the factors related to the fair value decline, including the impact on the fair value of ABI’s shares during the COVID-19 pandemic, which has negatively impacted ABI’s business.”... “Altria has evaluated the duration and magnitude of the fair value decline at March 31, 2021, ABI’s financial condition and near-term prospects, and Altria’s intent and ability to hold its investment in ABI until recovery.”

It appears that the global pandemic did play a role in the price drop of ABI, but this explanation doesn’t tell the full story, since the first price decline happened in October 2019, whereas the first acknowledgement of cases in Wuhan occurred on December 31, 2019 and the WHO declared a global pandemic on March 11, 2020. At the date of writing (June 2021), ABI’s stock price has increased, but has yet to return to its December 2020 price.

Where companies do record impairment, review the factors that led to the impairment and consider whether the write-downs are sufficient. Impairment can be a harbinger of trouble to come.

Operations

Quality products, services and business processes are the most important ingredient to a company’s success. Operational problems are insidious and can only be masked by accounting tricks for a short time. Look out for things like defects, recalls, a decline in the user base, and increasing returns.

Consider if a company’s description of their operations is consistent with what you see. The Luckin Coffee fraud was found by people counting customers at popular locations and realizing the revenue numbers (locations x customers x coffee prices) couldn’t possibly add up; Blink Charging Co is currently facing class action lawsuits because people noticed disrepair in charging stations that was inconsistent with management statements.

Finally, look for sudden changes in operations. Sometimes these changes are subtle, but if you look, you may be surprised at what you (or your algorithms) can find.

($BTBT | 2-F | December 2020) “The Company commenced its mining operations in February 2020 and we disposed of our former peer-to-peer lending business (the sole operation of the Company for 2019 and 2018, which ceased operation in October 2019) and the former car rental business in PRC on September 8, 2020.” “Initially, we were primarily an online finance marketplace, or “peer-to-peer” lending company, in China that provided borrowers access to loans. On October 24, 2019, the Pudong Branch of the Shanghai Public Security Bureau (the “Bureau”) announced that it conducted its investigation against Shanghai Dianniu Internet Finance Information Service Co. Ltd, which was a variable interest entity (VIE) of the Company, for suspected illegal collection of public deposits.”

Off-balance sheet

Off-balance sheet transactions are those that create risks or liabilities that aren’t represented on the face of the financial statements. Off-balance sheet transactions can take many forms including guarantees, operating leases, variable interest entities (VIEs) and joint ventures.

Joint ventures and other equity-accounted investments can be used to facilitate earnings manipulation. Management has an incentive to over-allocate expenses to entities that don’t get fully consolidated into their financial statement figures.

China has specific rules about foreign ownerships, and as a result, many companies operating in China must use VIEs to conduct their operations. There is variability in whether VIEs are included or excluded, leading to lower comparability and transparency.

Cash flow, credit, and bankruptcy

Cash flow statements are sometimes mistakenly considered “impossible” to manipulate. This is not the case. Management has some choice around what gets included in operating, investing, and financing sections. Differences in these classifications can make the cash flow statement misleading. Where negative cash flows from operations may signal that your business can’t support ongoing operations, spending in investing and financing sections can be spun as reinvesting in capital assets for future periods and paying down your debts.

Any cash-related pressures increase the likelihood of fraud. Malfeasance is much more likely in instances where the company is at the risk of bankruptcy. Fraud becomes more attractive when meeting your numbers is do or die.

Watch out for any members of the management team or the board who have been involved in bankruptcy proceedings in the past, especially where the bankruptcies came as a surprise. Bankruptcies happen, and sometimes great people are pulled in to help companies out in tough situations. Consider the context because previous involvement with a company that went to zero may be a red flag.

Regulatory, complaints, and legal

An investigation from a securities commission is a bad sign, but usually isn’t the first sign of trouble. Bad companies are often bad in more than one way, so consider all types of regulatory infractions in your assessment of a company.

Don’t disregard FCC complaints, OSHA investigations, and GDPR complaints. Frequent violations provide insight into management integrity, and issues with permits and approvals, environmental infractions, privacy violations, and others can provide insight into future changes to operations.

($CALM | 10-Q | March 2021) “The Egg Products Plaintiffs allege that the Company and other defendants violated Section of the Sherman Act 15. U.S.C. §1, by agreeing to limit the production of eggs and thereby illegally to raise the prices that plaintiffs paid for processed egg products.” “Plaintiffs assert that defendants violated the DTPA [Deceptive Trade Practices Act] by allegedly demanding exorbitant or excessive prices for eggs during the COVID-19 state of emergency.”

Additional factors influencing risk profile

Geographic

Despite its problems, the U.S. securities regulation regime and audit oversight process, is comparatively very strong. Many other jurisdictions lack strong regulatory regimes and for that and other reasons, companies that are domiciled abroad or that have significant international subsidiaries, are at a greater risk of earnings management, asset misappropriation and other types of malfeasance. Risks associated with bribery and corruption and other social and environmental risks also increase at companies with a large international presence.

While China is the jurisdiction most frequently associated with corporate fraud scandals, even Canadian and European companies tend to have slightly higher risk profiles due to a variety of regulatory differences.

Tax

Tax is complicated. There is a large amount of estimation and management judgment that goes into booking tax-related financial line-items. Deferred tax assets and the associated valuation allowances have long been used for earnings management. Like other reserves and provisions, management teams may over-allocate to valuation allowances in good years and reverse them in bad ones.

Look out for releases of valuation allowances that do not appear to be justified.

Tax havens

Businesses that are domiciled in tax havens, have significant transactions with companies in tax havens, or who have subsidiaries in tax havens, have a slightly higher risk profile. This should come to no surprise to anyone familiar with the Panama Papers scandal.

Strategy

Strategy descriptions that use the terms “high growth”, that are exclusively acquisition-centric, or that use overly aggressive or promotional language may indicate a higher risk profile.

Buzzwords & jargon

Fraudsters often lean on buzzwords and jargon. Watch out for sentences that use flowery language but in essence mean nothing.