When users of financial statements think about the business those financial statements belong to, they assume that the business will remain in business. This may seem painfully obvious, but it’s far more profound than just taking the future for granted. The assumption that a business will continue to do business in the future is one of the underlying principles of accounting. It even has a name: the going concern principle.

This post will explain the meaning of going concern and discuss what happens when there’s “substantial doubt” about a going concern and more.

What does it mean for a business to be a going concern?

In simple terms, for a business to be a going concern means that we assume that it will continue operating for the foreseeable future (usually the next 12 months unless otherwise specified).

So with that in mind, it’s a good thing for a business to be a going concern. To not be a going concern means that a business can’t pay its bills, and that means it will eventually go out of business, which is usually a bad thing.

A substantial doubt about going concern

Substantial doubt about an entity’s ability to continue as a “going concern” exists when there’s a real risk that the company might go out of business. In accounting speak, substantial doubt exists when it is probable “that the entity will be unable to meet its obligations as they become due within one year after the date that the financial statements are issued.” This is the definition under U.S. GAAP.

In other words, it means that the business faces the risk of a cash crunch or liquidity crisis in the next 12 months. This can be caused by insufficient revenue from operations to cover ongoing expenses, a large debt obligation coming due that the company may not be able to repay without additional funding or other cash flow pressures.

When conducting an audit of a company’s financial statements, it is the auditor’s responsibility to evaluate that company’s ability to continue as a going concern. If a substantial doubt exists, they must include an explanatory paragraph about this conclusion.

An audit report with this explanatory paragraph serves as a warning to its readers about the company’s financial health.

In the U.S., the company’s management team also has a responsibility to assess the entity's ability to continue as a going concern. Note that sometimes the company will disclose that they evaluate the risk of a going concern issue and concluded there was none. In this instance, investors and stakeholders should review management’s disclosure to determine whether the justification for the conclusion is robust.

Where to find information on the going concern status of a company

If an issue exists, a warning will be included in the audit report. The going concern paragraph will appear directly after the auditor’s opinion paragraph under a suitable title (e.g., “Assessment of the Company’s Ability to Continue as a Going Concern” or simply “Going Concern”). Per PCAOB auditing standard 2415, the conclusion in this paragraph should include the phrasing that includes both “substantial doubt” and “going concern.”

You can find management’s assessment of this risk in the 10-K annual report, generally in the Management Discussion and Analysis section.

Hudson Labs is the only platform that provides real-time and comprehensive reporting on going concern warnings. While you can use EDGAR full-text search to find mentions of “substantial doubt” and “going concern,” such a search will include many false positives.

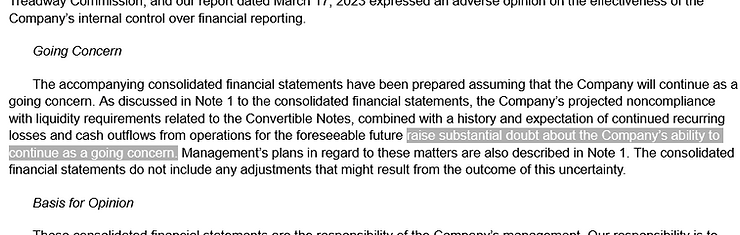

Example of a going concern warning (substantial doubt about going concern)

Here is an example of a recent auditor report that includes a going concern paragraph:

Note that the going concern paragraphs refers readers to the notes to the financial statements for more details regarding the specific strains on their cash flow.

How common are going concern warnings?

As you may expect, going concern warnings are highly unusual among large cap companies. Companies with large valuations usually got there by generating ample cash from operations. On the other hand, small and micro cap companies are less likely to have proven business models and are more likely to rely on external funding rather than cash from their own operations. This means smaller and newer companies are much more likely to see these warnings.

Data gathered and analyzed by Hudson Labs found that in 2022, approximately:

- 40% of micro cap companies

- 20% small cap companies

- 2% of mid cap companies, and

- Less than 1% of large cap companies

expressed doubt about the company’s ability to continue as a going concern.

Macro-economic events and sector trends can also lead to an increased incidence of going concern warnings overall. For instance, in September 2022, we identified that 40 percent of companies that went public via merger with Special Purpose Acquisition Company (de-SPACs) had going concern warnings. Here is the Bloomberg coverage of the Hudson Labs analysis.

Does substantial doubt about going concern increase bankruptcy risk?

The short answer is, yes. Obviously, a company that may not be able to meet its obligations in the next 12 months, is a company that is at risk of bankruptcy. It’s therefore no surprise that multiple studies have shown a positive correlation between going concern warnings and increased bankruptcy risk.

Conclusion

The going concern principle is one of the core concepts underlying accounting and financial reporting. Whenever an auditor or management team warns of “substantial doubt” about a company’s ability to continue as a “going concern”, users should always take notice. A going concern warning indicates that the business may soon not be in business, so be aware of the risk you’re taking before you invest.