One of the Securities and Exchange Commission’s (SEC) primary responsibilities is to review securities filings (e.g. prospectuses and annual reports) of public companies. Naturally, issues arise from the reviews performed by the SEC staff, and that often requires correspondence with the company that submitted the filing. These are commonly known as SEC comment letters. They are also sometimes referred to as “UPLOADs” which is how they appear on EDGAR.

This post will explain the types of SEC comment letters, their contents, where to find them, common topics, and more.

The Division of Corporate Finance

First, some background. The SEC has five divisions. The Division of Corporate Finance (DCF or “The Division”) is responsible for reviewing securities filings.

What is an SEC comment letter?

DCF issues comment letters in response to a public company’s filings. DCF staff issues a comment letter if it believes a company can better comply with a particular accounting rule or disclosure. The comment letter often contains a list of items that request:

- Additional information or disclosure

- A modification to the filing or disclosure

- That the company changes how it discloses something in a future filing.

If a company does not understand a comment, it can ask for clarification before responding. The company must reply to each item in the letter and, if appropriate, amend its filing. Often, the company’s explanations will resolve the comments. However, depending on the nature of the issue and the company’s response, DCF may have further comments and requests for information. The SEC may then decide to follow up again until the matter is resolved.

At any time during the review, the company may ask that DCF staff reconsider a comment or its view of the company’s response to a comment.

SEC comment letters are made public no sooner than 20 business days after it has completed its review.

Is an SEC comment letter a red flag?

It’s also worth noting that certain filings are always reviewed by DCF, including Form S-1, which is the form filed when a company officially registers to become a public company. So in that instance, a comment letter is not unusual, and it will likely contain insights on what the SEC finds noteworthy in the filing. Likewise, how the company responds to the Division’s comments will be insightful.

In general, the SEC website explains that DCF:

concentrates its review resources on disclosures that appear to be inconsistent with Commission rules or applicable accounting standards, or that appear to be materially deficient in their rationale or in clarity.

This means that comment letters can uncover a range of issues from minor issues with form or format to egregious issues that require restatement. For instance, Credit Suisse restated their cash flow statements after a series of queries from the SEC in early 2023, prior to their collapse.

At best, the DCF will issue a comment letter if it believes a company’s accounting or disclosures need further explanation or need to be stated more clearly. At worst, the staff may believe that the accounting doesn’t comply with GAAP or the disclosures don’t follow SEC rules, like the Credit Suisse example above. Regardless, a comment letter is something that companies have to take seriously and respond to, so there’s always a chance that their contents might contain something of interest to investors.

Examples of SEC correspondence

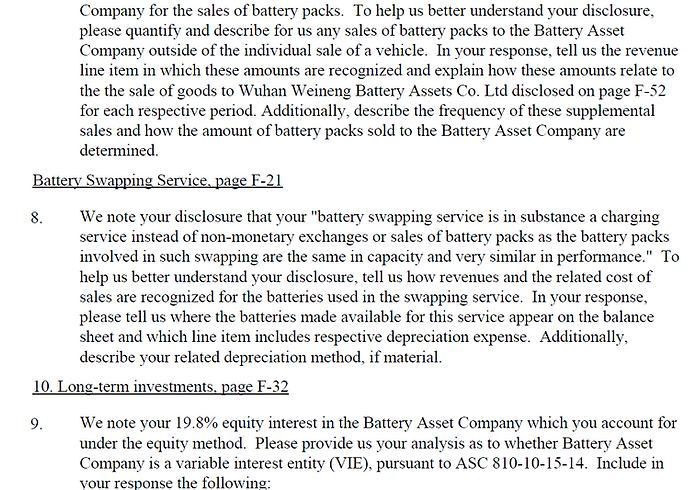

Below is an excerpt from an SEC comment letter sent to NIO, Inc. (NIO) in September 2022 related to its revenue recognition for one of its segments:

In the second paragraph of the letter, DCF requested a response “within ten business days,” and NIO responded with a request for an extension of time to provide a full response. Requests for extension are very common, and NIO followed up with its complete response approximately a month later.

For this particular exchange between NIO and DCF, there were a total of four items,

- The initial SEC comment letter

- Two responses from NIO

- A response from DCF that it had completed its review.

The correspondence was made public about a month after it had concluded.

Where to find SEC correspondence

Historically, locating SEC comment letters hasn’t been easy. SEC comment letters are filed as PDFs and are hard to find because they’re listed at the date they were sent, not the date they were made public. With Hudson Labs, you can find SEC correspondence right in your news feed or from the company page with a single click. Users can also receive daily alerts on SEC Comment Letters alongside other risk feeds.

Hudson Labs SEC comment letter feed:

Hudson Labs Twitter company page - SEC correspondence view

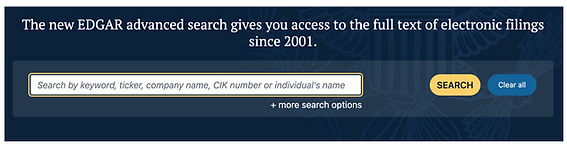

Finding SEC correspondence using EDGAR

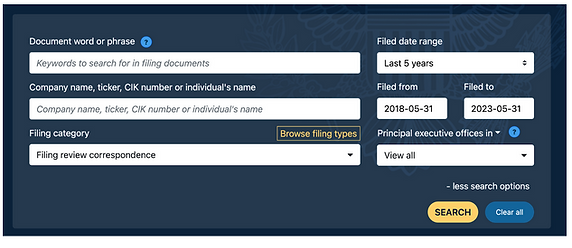

Of course, you can also find SEC comment letters using EDGAR search, which has improved over the years. Simply click on “more search options”:

Then click the “Filing category” drop-down menu, and select “Filing review correspondence.” To review correspondence for a specific company, include the company name or ticker symbol in the field above the “Filing Category” field.

For more tips and tricks on navigating EDGAR, read “How to Become an EDGAR Power User”.

UPLOAD and CORRESP filings on EDGAR

When EDGAR spits out the search results for filing review correspondence, you’ll note two main types of filings:

- UPLOAD—These are letters that originated with the SEC.

- CORRESP—Responses from the filing company.

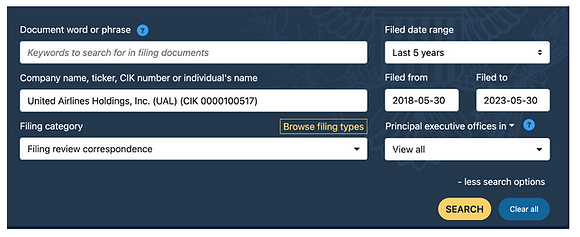

Here’s another screengrab using United Airlines:

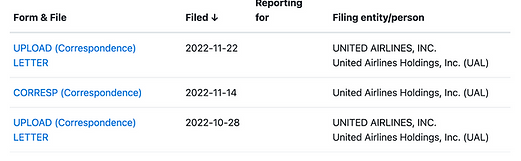

Below are the first three results from that search:

The November 22, 2022, UPLOAD is an SEC letter notifying the company that their review is complete.

You can also find the same information by navigating directly to the United Airlines company page on EDGAR. For instructions on using the “Company Search” functionality of EDGAR, refer to our post “How to Become an EDGAR Power User”.

Common topics for SEC comment letters

The precise nature of SEC comment letters is closely tracked, particularly by advisors to public companies and research firms, including Hudson Labs. Each of the Big 4 accounting firms—PwC, Deloitte, EY, KPMG— regularly analyzes trends in SEC comment letters.

Based on a review of recent analysis, in no particular order, the most common topics of SEC comment letters are:

- Non-GAAP metrics

- Management’s Discussion and Analysis

- Segment reporting

- Business combinations and acquisitions

- Climate change matters

- Revenue recognition

- Fair value accounting

- Inventory and cost of sales

- Internal controls over financial reporting

Recently, many SEC comment letters have noted differences and discrepancies between a company’s SEC disclosures for climate change and disclosures made elsewhere (e.g., Corporate Social Responsibility reports, investor presentations, and information on websites).

Although not a real-time source of information, SEC comment letters provide insight into what accounting and disclosure areas are of interest to the Commission. In some instances, like Credit Suisse and NIO, the SEC correspondence can help stakeholders hone in on real risks to the business and to earnings quality.

Hudson Labs makes SEC comment letters easy to find as soon as they’re filed, as well as by a specific company. With such straightforward access, these letters and their contents provide users with another tool to make better investing decisions. Every week, we highlight SEC Commentary to our users that often leads to price-moving changes in related party disclosure, KPI reporting, corrective statements, and more. Users can also receive daily alerts on SEC Comment Letters alongside other risk feeds.