The following are the thoughts and opinions of Kris Bennatti and do not reflect those of Hudson Labs or the rest of the team.

I work out of a WeWork (my favourite de-SPAC with a 70+ Bedrock risk score) in downtown Toronto with a bunch of other founders with millions in uninsured deposits.

Despite my reputation as a fraud-finding hard-headed traditionalist, many of my friends are building “blockchain-enabled cockfight marketplaces” and “NFT valuation chatbots”. I occasionally get invited to parties like this one.

I can feel your hatred seething from the page and I haven’t even hit send yet.

It’s okay because I’m mostly kidding. In reality most of us run pretty normal businesses that happen to be venture-backed. Like most founders, my business is my life and my passion. If I lost Hudson Labs it would break my heart and put eight people out of work.

Here’s what’s been happening in startup land.

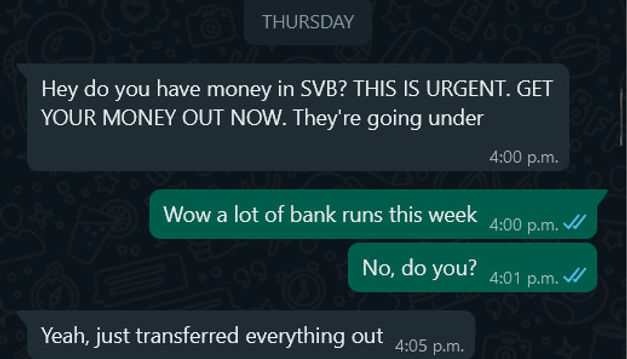

Thursday:

At 4pm I got this message from a friend:

About an hour later, another friend walked over to ask me if I knew what was happening. He had $3M sitting in a bank account in SVB. He started setting up accounts at Mercury and Brex. He attempted to transfer their deposits out but was unsuccessful.

Slack channels, WhatsApp groups and startup internet forums started blowing up with panicked chatter. Y Combinator (and Founders Fund to a lesser extent) are so large and fund so many companies, that a single post on a slack channel, forum or sent through email is instantly seen by thousands of business owners and in cases like this, quickly shared even farther.

We bank at a stodgy Canadian bank but even so, I felt sick with empathy pain.

On Thursday, a lot of people were learning about FDIC insurance limits for the first time. One forum post the next day noted, “We’d like to set up a bunch of accounts with banks with over 100b in assets up to the $250k limit.”

Anecdotes heard through the grapevine:

- A founder located in Mexico city flew to San Francisco because he thought showing up in person might help.

- Another founder withdrew multiple millions in the form of a cashiers check and essentially had it under his mattress until he could cash it on Monday.

The aftermath:

The FDIC announcement has only partially stemmed the panic. Our friends who have U.S. corporations are still thinking of moving away from whatever bank they're using to a top five bank.

Initially Brex, Mercury and other popular neo banks got a huge lift as companies panic transferred out of SVB to anything else. It seems like that lift might be temporary as founders opt for the safest possible choice.

I’ve been getting a LOT of questions from family, friends, customers and reporters. Here are some of the top questions and my thoughts.

1. Which bank is next?

Hopefully Signature was the last? Hold on to your hat.

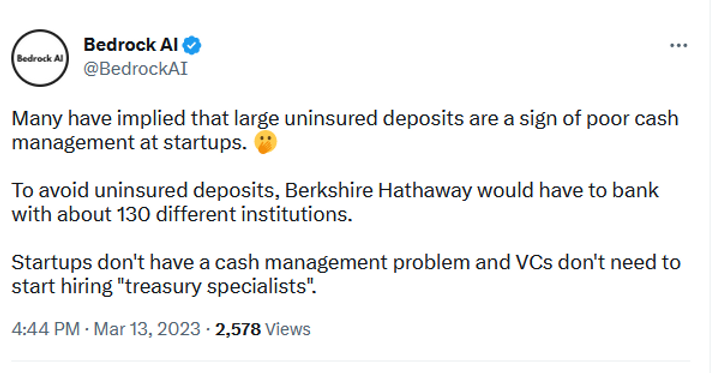

2. Are tech founders bad at risk management/cash management?

Opening a checking account at SVB does not even rank on the spectrum of startup risk.

It’s normal for businesses to have large uninsured deposits. It’s also normal for small businesses to only bank with one bank. If you don’t, cash management becomes more complicated. Depositing your money in a big 40-year old FDIC insured bank isn’t exactly poor risk management.

3. Is Hudson Labs going to start banking with multiple banks now?

No, when there’s a run on a top 5 Canadian bank, there will be zombies in the streets and it won’t matter anyway.

4. Why did SVB and Silvergate have low Hudson Labs risk scores?

Because they weren’t committing fraud.

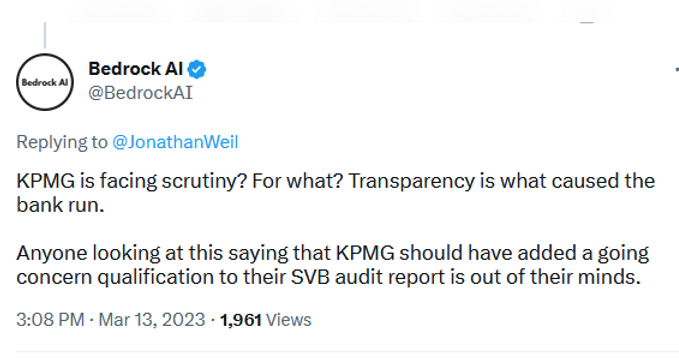

5. Why did KPMG give SVB a clean audit opinion?

I presume it was because the financial statements were free of material misstatement and fraud. What do people think auditors do?

SVB was a going concern at the date of the audit report. My thoughts and prayers are with SVB audit partner, Tarek Ebeid who will be put through hell over the next year for no good reason.

But seriously, the risks to SVB were clearly disclosed. If they weren’t, there wouldn’t have been a run on the bank. I assume that no one other than Andre who wrote this tweet is much upset about the SVB note tie out not matching.

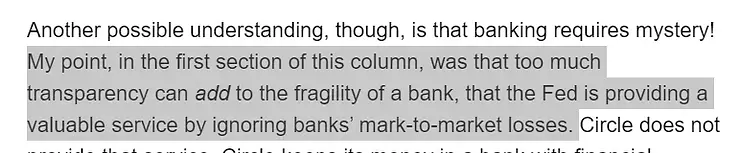

Here’s a tongue in cheek comment from Matt Levine’s Money Stuff yesterday. We both agree that transparency in financial reporting wasn’t the problem:

Coincidentally, I was once part of a KPMG audit team that failed to add a going concern qualification right before our client went bankrupt. My working papers got subpoenaed. Life is funny.

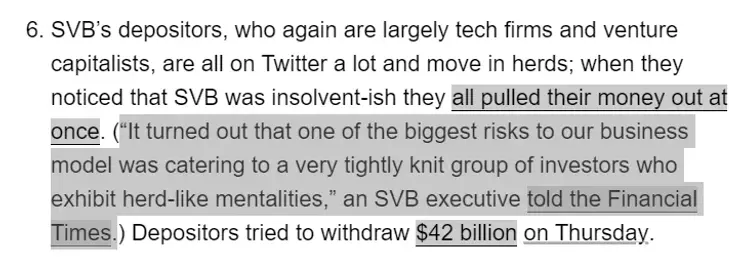

Also from Levine re: the tech herd mentality:

I took a course on Risk Management in Financial Institutions during my masters degree with the great Lois Tullo. During the course, we met with the CROs of four of the big five Canadian banks and heard them talk about their approach to risk management. I was surprised by how fluffy FI risk management is/needs to be. Quantitative measures of risk and sensitivity analysis don’t account for risks like a user base that’s tight knit and moves in a pack. A CRO’s job is to imagine sci-fi type, black-swan situations and prepare the bank for them the best they can.

Shame on SVB for not taking the office of CRO very seriously.

One last thought - banks used to fail a lot more frequently. The last few weeks were a lesson in the value of central banking. I highly recommend listening to this Planet Money podcast, “A locked door, a secret meeting and the birth of the Fed”. It shows what crises like these looked like before the Fed. JP Morgan locked a group of bankers in a room in his house until they got their shit sorted. The health of the U.S. financial system was dependent on the power and influence of one man. For more of my favourites, see “All-time best podcast episodes about markets and investing”.

I’d say more about SVB but everything smart that needed to be said, has already been said by Matt Levine and a few others. And despite my CPA designation and one relevant masters course, I’m not a financial institutions expert. There are enough self-appointed experts on Twitter for me to safely sit this one out.